.")

Due to the existing excess and incoming supply, as well as the fact that supply continues to outstrip demand, it is projected that rental rates and occupancy levels for office buildings in the Klang Valley would continue to decline in the second half of the year (2H2022).

The country’s rapid economic expansion is anticipated to have a favourable effect on the office market, though. The Edge | Knight Frank Kuala Lumpur and Selangor Office Monitor 2Q2022, presented by Knight Frank Malaysia executive director of corporate services Teh Young Khean, predicts that as business sentiment and trade gradually improve, demand for office space will rise over time, stabilising occupancy and rental levels.

“Having a physical office is still crucial to businesses since it symbolises and emphasises the company culture and brand, despite the recent trend of working from home. Since it appears to have a higher favourable effect on one’s physical and mental wellbeing, a physical workplace is still essential for collaborative work and to foster a sense of belonging for employees, Teh notes.

According to him, landlords who successfully modernise their office complexes by providing greater collaboration areas and flexibility will probably draw in more tenants. To create a decent balance between comfort and productivity, organisations are redefining how the office operates by introducing a small amount of the home element.

E-commerce platforms will also keep expanding as more people get involved in these firms. Their expansion would also benefit related industries like call centres and customer service departments. Software developers, e-wallet platforms, and other tech enterprises such as digital banks will also have growth potential, according to Teh.

He observes that as environmental, social, and governance (ESG) awareness rises, more office renters are also expressing a strong interest in green structures. Tax incentives that support the Sustainable Development Goals of Agenda 2030 are available for green buildings that have been certified by the Malaysian Green Technology Corporation (SDGs).

“Overall, there will be more rivalry in Kuala Lumpur’s office market due to the upcoming supply of around 5.33 million sq ft of office space by 2H2022. The Selangor office market is anticipated to hold up well in the meantime thanks to an increase in leasing activity.

Average rental rates remain mostly unchanged

Teh asserts that the entry of Malaysia into the Covid-19 endemic phase on April 1 revitalised a number of economic sectors. This is advantageous for both the real estate market and the nation’s economic recovery.

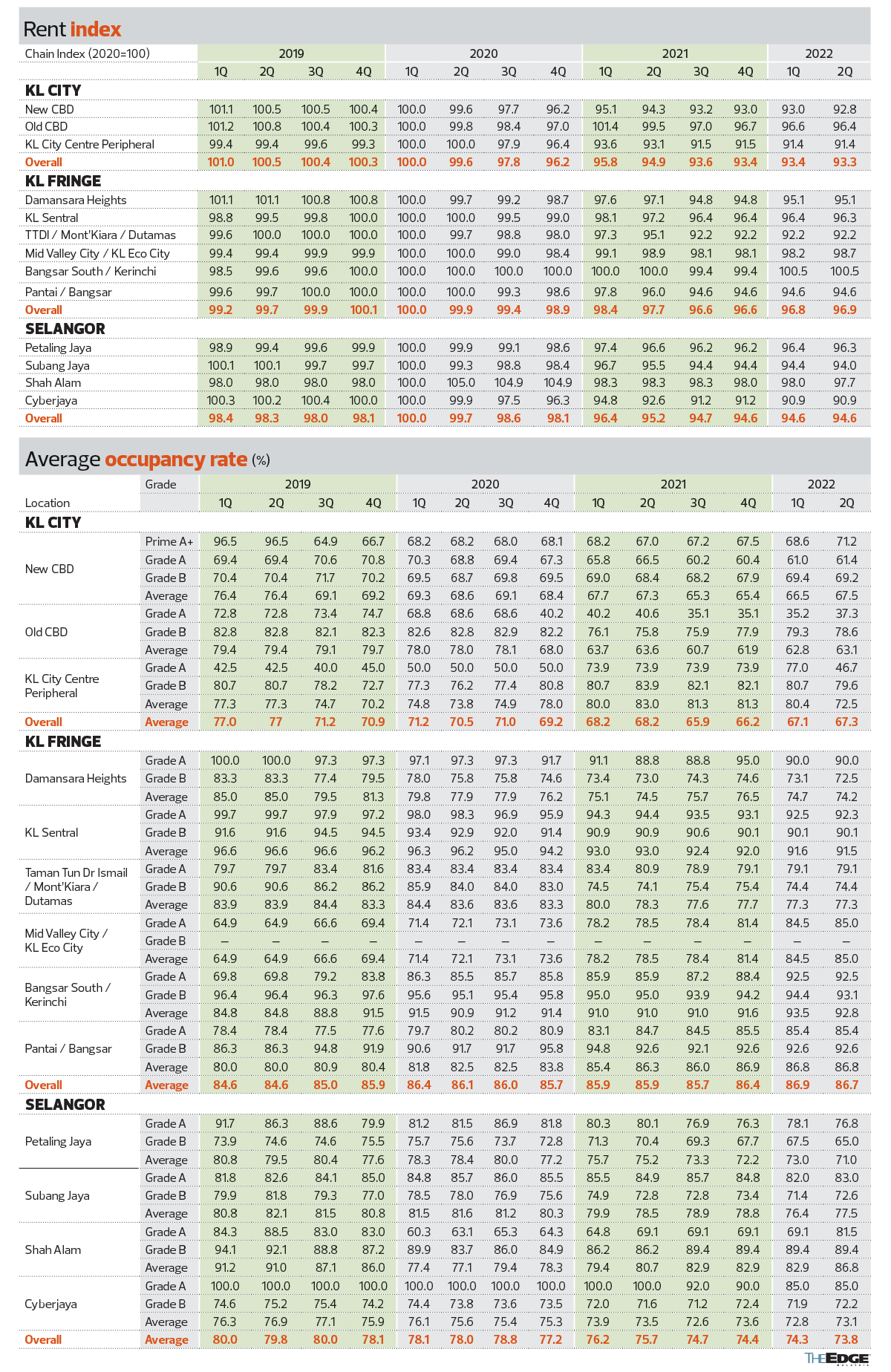

“As more workers gradually return to the workforce, the pace of recovery in the office sector will continue to accelerate in the second half of 2022. Overall occupancy rates for KL city, KL fringe, and Selangor throughout the quarter varied just little, plus or minus 0.2%. Despite this, the Klang Valley office market is still favourable for renters, according to him.

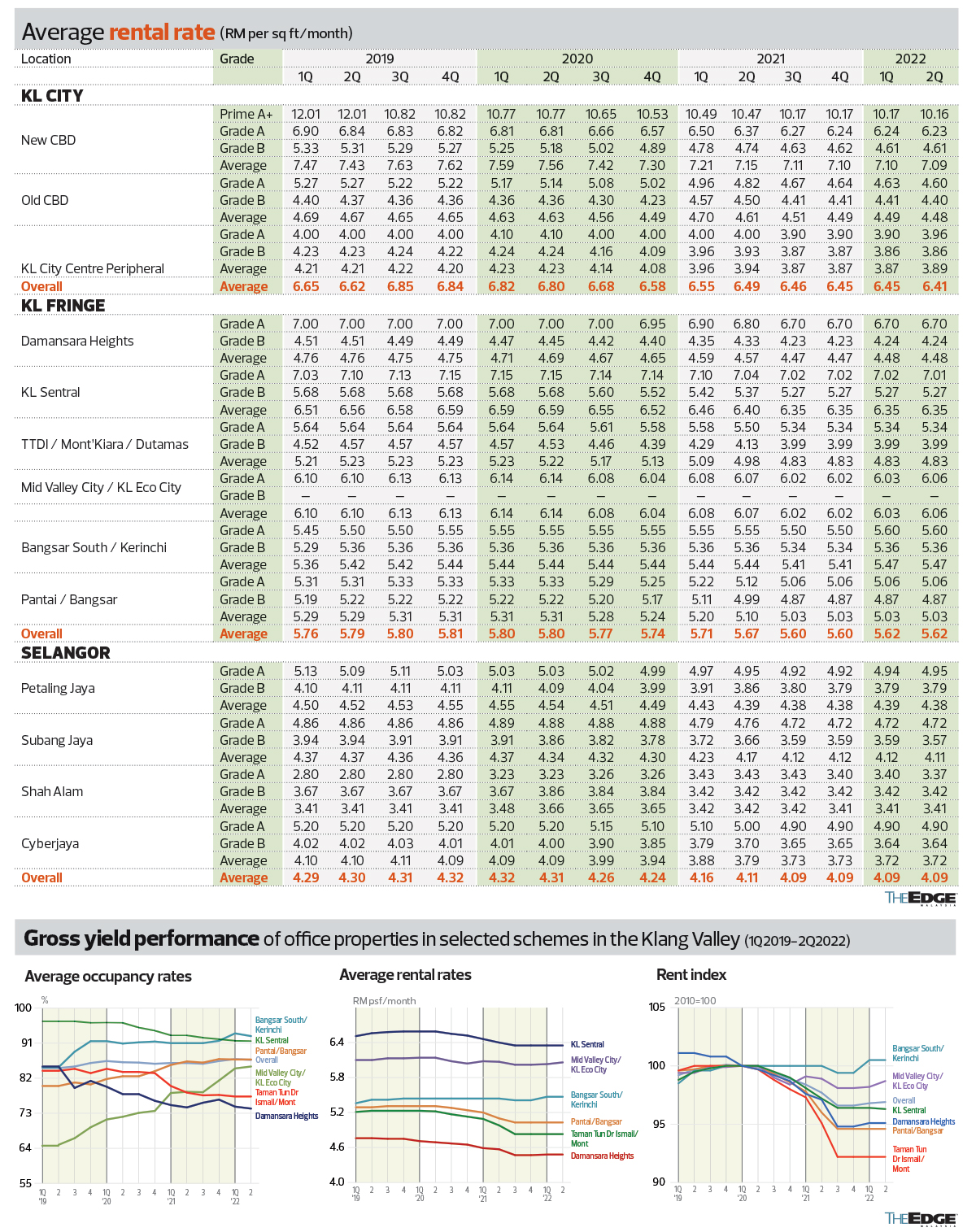

In KL City’s new CBD and old CBD, the average rental rate for Prime A+, Grade A, and Grade B offices declined marginally from quarter to quarter (q-o-q) to RM7.09 and RM4.48 psf, respectively, while it climbed by 0.5% to RM3.89 psf in the city centre peripheral.

With the exception of Mid Valley City (MVEC)/KL Eco City (KLEC), where the average rental prices for Prime A+, Grade A, and Grade B workplaces climbed by 0.5% to RM6.06 per square foot. The rates were the same from one quarter to the next in Damansara Heights, KL Sentral, Taman Tun Dr Ismail (TTDI)/Mont’Kiara/Dutamas, Bangsar South/Kerinchi, and Pantai/Bangsar at RM4.48, RM6.35, RM4.83, RM5.47, and RM5.03 psf, respectively.

The aggregate rental rates in Selangor were constant in 2Q2022. Average rental rates in Petaling Jaya and Subang Jaya decreased slightly to RM4.38 psf (1Q2022: RM4.39) and RM4.11 psf, respectively (1Q2022: RM4.12). Shah Alam and Cyberjaya’s respective rents remained constant at RM3.41 and RM3.72 psf.

The average occupancy rate in KL city as a whole increased marginally by 0.2% to 67.3% during this time. The occupancy rates for the KL city centre peripheral declined significantly to 72.5% (-7.9%) q-o-q, while the occupancy rates for the new CBD and old CBD were higher, at 67.5% (+1%) and 63.1% (+0.3%), respectively.

Only MVEC/KLEC had an increase in occupancy rates, which brought the average occupancy rate in KL periphery up to 85%. At 77.3% and 86.8%, respectively, TTDI/Mont’Kiara/Dutamas and Pantai/Bangsar remained constant. KL Sentral, Bangsar South/Kerinchi, and Damansara Heights saw declines to 74.2%, 91.5%, and 92.8%, respectively.

Selangor’s overall occupancy rate decreased from 74.3% in the first quarter of 2022 to 73.8% in the second. Petaling Jaya’s average occupancy rate fell by 2% to 71%, while occupancy rates increased in Subang Jaya, Shah Alam, and Cyberjaya to 77.5%, 86.8%, and 73.1%, respectively.

Kuala Lumpur saw an increase in net absorption of about 347,307 sq ft in the second quarter of 2022.

During the time period under consideration, Selangor also saw positive net absorption of about 22,044 square feet.

KL city now has an estimated supply of 57.25 million square feet of office space, followed by KL fringe (28.59 million square feet) and Selangor (25.53 million sq ft). The total now stands at 111.37 million square feet.

Currently, KL city leads with 4.57 million square feet of the 9.28 million square feet of office space that is being built, followed by KL fringe (2.82 million square feet), and Selangor (1.89 million sq ft). Over the next 22 years, Knight Frank Malaysia anticipates an increase in office space of 8.3%.

Source from TheEdge